Dear NAPCP Members,

We know everyone has been inundated with numerous amounts of information regarding federal, state, local, and private options for financial help during this unprecedented time. You probably have realized that the information appears to change every day. We have listed for our members below what we have found out regarding the Federal, State, Local and private financial options for small businesses and owners. But please do your due diligence regarding anything you see listed here and anywhere else because many of the non-federal options may be specific to your state or local areas.

INTERNATIONAL PROGRAMS

Government Relief Programs Around the World

It is not a complete list but they state they are updating the list when information becomes available.

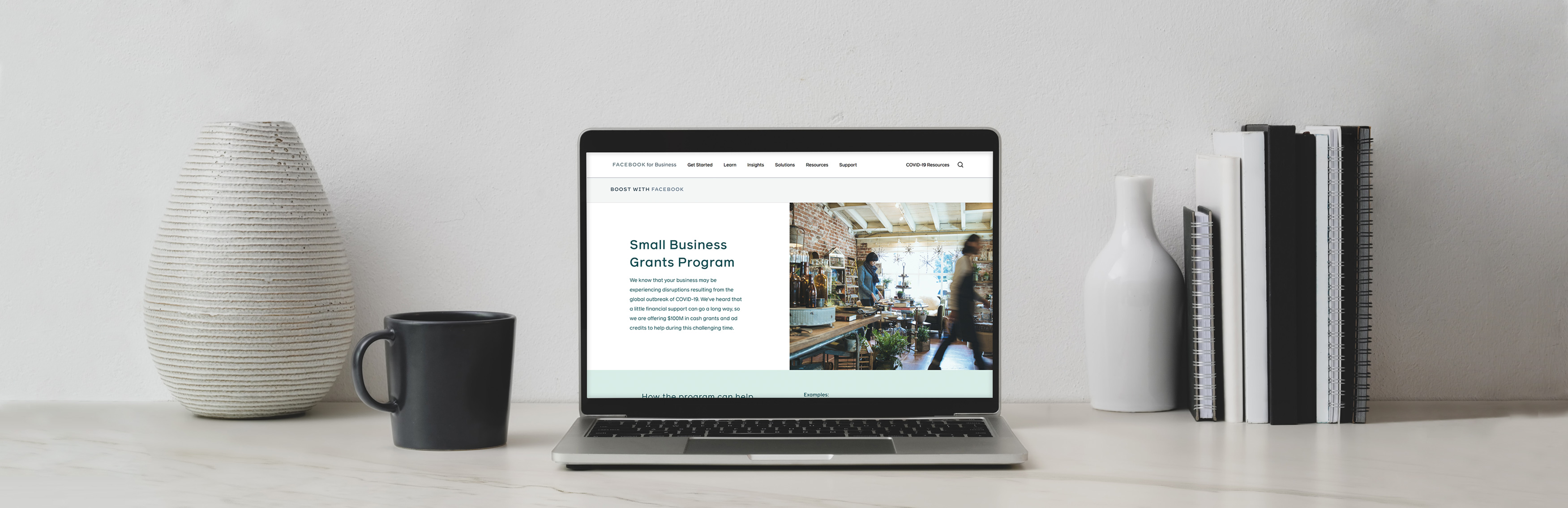

Private Financial Program from Facebook

Offering $100 million in Cash Grants and Ad Credits to small businesses. Program is available in over 30 countries.

DOMESTIC PROGRAMS

National Governors Association

Find out what state programs are being offered.

Community Foundation Locator

Community funds, residents are donating money to help locals and local businesses in need. Use the link to see if there’s a foundation raising money in your area.

STIMULUS CHECKS

The $2 trillion Coronavirus Aid, Relief, and Economic Security (CARES) Act includes direct payments to most Americans.

A Social Security number is required to receive a payment, reports the Wall Street Journal.

According to pages 144 and 145 of the 880-page rescue plan, nonresident aliens, those who can be claimed on someone else’s tax return as a dependent, and estates or trusts are all excluded.

In addition, an earnings threshold based on adjusted gross income will mean no checks for some Americans.

How Much Money Will I Receive?

The coronavirus relief package provides direct cash payments of up to $1,200 for most adults — or $2,400 for married couples filing jointly — plus $500 per child under 17.

To get the full amount, your adjusted gross income on your 2019 tax return (or 2018, if you haven’t already filed for 2019) must not exceed the following:

- Individuals: $75,000

- Head of Household: $112,500

- Joint Return (Married Couples): $150,000

(Note: Find your adjusted gross income on line 8b of Form 1040)

If you make too much money to receive the full amount, you may still receive a smaller check. Reduced stimulus payments will go out to individuals who make up to $99,000 and married couples who make up to $198,000.

What if I Don’t Normally File a Tax Return?

Senior citizens, Social Security recipients and railroad retirees who are not otherwise required to file a tax return are eligible to receive an economic impact payment.

The Treasury Department and IRS previously said these groups would need to file a “simple tax return,” but that’s no longer the case.

“Social Security recipients who are not typically required to file a tax return do not to need take an action, and will receive their payment directly to their bank account,” said Treasury Secretary Steven Mnuchin.

The IRS will use the information on the Form SSA-1099 and Form RRB-1099 to generate $1,200 payments to Social Security recipients who didn’t file tax returns in 2018 or 2019.

Recipients will get the payments as a direct deposit or by paper check, just like their regular benefits.

For other people who don’t file taxes — including those with no income — the IRS has set up a new website where you can enter your payment information. Follow this link to get started.

When Will I Receive My Stimulus Payment?

The government deposited the first wave of payments into taxpayers’ bank accounts on April 11, according to a tweet from the IRS.

Treasury Secretary Steven Mnuchin said on April 2 that payments should begin to show up in bank accounts in about two weeks, according to USA Today. For those without direct deposit, he said it should be a matter of “weeks.”

How Will I Receive My Check?

If you gave bank information to the IRS on your 2018 or 2019 taxes, the payment will be made electronically.

For those who don’t have direct deposit set up with the IRS or have changed banks, you could be waiting longer for your payment to be issued by mail. It will be sent to the address on file with the IRS.

However, a web-based portal is being developed to allow people to give bank information to the IRS and get their payment faster. Follow this link for updates.

Do I Have to Sign Up to Receive a Stimulus Payment?

There’s no need to sign up for anything. The government will determine your payment eligibility and amount by reviewing your tax returns or Social Security benefit statement.

You’ll be notified by mail no later than 15 days after the payment is distributed, according to page 149 of the relief package.

What if I Haven’t Filed My 2018 or 2019 Taxes?

Since the IRS is relying on 2018 or 2019 tax returns to determine the payments, anyone with a tax filing obligation is urged to file as soon as possible. Make sure to include direct deposit banking information on your return.

Do I Have to Pay Taxes on the Payment?

The money that you receive from the CARES Act is not considered taxable income, according to Forbes, MarketWatch and other major news sources that we checked.

Will There Be an Additional Stimulus Payment?

This is a one-time payment, but the Trump administration has not ruled out additional economic relief packages in the future.

Where Can I Go for More Information?

There are some questions that can’t be answered at this time, but the IRS has set up a special website that you can check for updates. The IRS is asking people to avoid calling them about the stimulus payments.

UNEMPLOYMENT INSURANCE

Please refer to your state Labor department. I believe that each state department has now implemented their own regulations and guidelines for self employed and small business owners. For example, in Georgia, self employed and certain small business categories were normally not allowed for unemployment Insurance but they have made exceptions for all self employed and small business owners.

The new law expands unemployment benefits dramatically, with an additional federal payment boosting normal benefits. Here are the details:

- In addition to normal state benefits, an additional $600 per week will be paid to individuals for up to four months. This boost will help individuals earn around the median weekly wage.

- Benefits will last longer too. Regular state unemployment eligibility of 26 weeks has been expanded by an additional 13 weeks, for a total of 39 weeks.

- The package expands unemployment insurance to those who don’t typically qualify: Gig economy workers who are classified as independent contractors and self-employed individuals.

- Individuals who haven’t been laid off, but can’t work due to a variety of reasons related to COVID-19, would also be eligible for unemployment checks. These reasons would include a case where they were diagnosed with COVID-19, were awaiting a diagnosis, or had a family member diagnosed with the disease; Individuals who were scheduled to start a job and could not because their future workplaces had been shut down due to the COVID-19 pandemic, would also be eligible. Additionally, individuals whose head of household died directly due to COVID-19 will be eligible.

- Workers who are furloughed, but haven’t been fully laid off, are eligible.

- The 7-day waiting period before an unemployed worker can get benefits, which is a standard feature of most states’ unemployment systems, is being waived to help individuals receive cash as quickly as possible.

If you’re considering filing for unemployment, there are other provisions experts recommend considering first, like exhausting paid sick leave (which could end up paying you more than unemployment insurance). Keep in mind there are already reports of unemployment offices experiencing an overwhelming number of calls, which might stall the process of enrolling and receiving payments.

MORTGAGE AND RENTER RELIEF

Borrowers with federally backed mortgage loans—loans under Fannie Mae and Freddie Mac—who are experiencing financial hardship due to COVID-19 can request forbearance on their payments for up to six months. Borrowers must submit a request to their servicer and affirm that they’re experiencing a financial hardship during the crisis. Additionally, no foreclosures or evictions from properties with federally backed mortgages can occur during this period.

During the mortgage forbearance period, interest will still accrue. However, additional fees, penalties or extra interest cannot be added to mortgages.

Renters have some eviction protection, but only if they live in a multifamily building or single family home that has a federally backed mortgage. Landlords cannot evict tenants of these buildings or charge any late fees, penalties or other charges for late rent payments.

FEDERAL CORONAVIRUS SMALL BUSINESS RELIEF PROGRAMS

What’s in the Coronavirus Relief Package for Small Businesses?

First, it’s important to note that for the purposes of this package the federal government is defining “small business” as a business with 500 or fewer employees. To qualify for the programs listed below, your business is going to need to meet the standards set forth by the U.S. Small Business Administration.

There are four federal programs now open to businesses affected by the COVID-19 crisis:

- The Paycheck Protection Program: This new program provides forgivable loans of up to $10 million to help businesses (and not-for-profits) with 500 or fewer employees keep their workers on the payroll. The loan can cover expenses including wages, rent, mortgage interest and utilities. The program is administered by the U.S. Small Business Administration (SBA) and is available through June 30, 2020. Loans are issued through private banks and backed by the government.

- Economic Injury Disaster Loans (EIDL): Also administered by the SBA, these loans can provide up to $2 million to businesses with 500 or fewer employees for a loan term of up to 30 years. An advance of up to $10,000 is available to applicants, and it does not have to be repaid.

- SBA Express Bridge Loans: These loans are only available to those with an existing business relationship with an SBA lender. They can give businesses quick access to up to $25,000.

- SBA Debt Relief: For six months, the SBA will automatically pay the principal, interest and fees on current qualified loans and new qualified loans issued before Sept. 27, 2020. The SBA is also providing automatic deferments through Dec. 31, 2020 on any currently serviced disaster loans.

Applications and details for the SBA programs can be found on its coronavirus relief resource page. Below are some more details regarding the Payroll Protection Program (PPP) and the Economic Disaster Loans and Advance (EIDL).

Paycheck Protection Program (PPP)

The federal Paycheck Protection Program was created as part of the Coronavirus Aid, Relief and Economic Security (CARES) Act to help businesses cover payroll and other expenses while they’re affected by the spread of the coronavirus.

Eligible businesses can qualify for Paycheck Protection Program loans of up to $10 million. The loans can be forgiven if a business maintains its payroll for eight weeks at employees’ regular salary levels and uses the loan proceeds for qualifying purposes. Other than payroll, acceptable uses of Paycheck Protection Program funding include rent, mortgage interest payments and utilities. But only 25% of the loan’s forgiven amount can cover non-payroll costs.

As of April 3, small businesses and sole proprietors could apply for funding, and independent contractors and self-employed individuals can apply beginning April 10.

This program will allow for small businesses to keep paying their employees even if the operation is shuttered due to the coronavirus pandemic.

This is done by issuing SBA loans to eligible businesses that come with the federal government’s promise to both defer payments and then forgive the loan as long as conditions are met.

The Paycheck Protection Program, which will be available for application beginning April 3, 2020, is supposed to have a more streamlined application process that could extend beyond typical SBA lenders.

Here’s what the SBA says about applying for it:

“You can apply through any existing SBA 7(a) lender or through any federally insured depository institution, federally insured credit union, and Farm Credit System institution that is participating. Other regulated lenders will be available to make these loans once they are approved and enrolled in the program. You should consult with your local lender as to whether it is participating in the program.”

Many banks and credit unions have closed their lobbies due to virus concerns, so if you go that route you may need to call ahead to set up a time for an appointment or a virtual consultation. There are many banking institutions participating in the PPP so check all your options: National Banks, Regional/Local Banks, Credit Unions, and Online Lenders.

What Small Businesses Need to Know About the Paycheck Protection Program

Eligibility Requirements

According to a guide for this legislation published by the U.S. Chamber of Commerce, the following are general guidelines for businesses eligible for access to the $350 billion dollars allocated to these federally guaranteed loans:

- Business or non-profit with fewer than 500 employees (this includes full-time, part-time and otherwise classified employees)

- Individuals who operate as a sole proprietorship, independent contractor or self-employed who regularly carry a trade or business.

If you’re unsure if you qualify, there is an online size standards tool on the SBA website to help you find out.

How Much Can I Borrow?

These loans can be for up to $10 million, but the amount that can be forgiven is measured by the eight weeks of prior average payroll plus an additional 25% of that amount, per the SBA.

Payments are deferred for six months on these loans, and small businesses could have up to 100% of the loan amount forgiven by the government if the money goes toward certain expenses

What Expenses Are Forgiven With This Loan?

If you use the money to maintain a workforce, the SBA will forgive the amount of the loan that is utilized in covering the first eight weeks of payroll.

Rent or mortgage payments on commercial property, mortgage interest and utilities also are 100% forgivable for this period.

If you use the money for something other than these things, you’ll have to pay for the loan. But it’s at an extremely low interest rate (0.5%) and payments are delayed for six months. The loan must be paid back in full within two years.

Caution: small business owners will want to take extreme care in documenting all of the expenses paid with this loan to ensure you get the maximum amount forgiven.

Disaster Loans and Loan Advances

Economic Injury Disaster Loans can provide working capital in short order for whatever a company’s needs may be.

The SBA is making these working capital loans of up to $2 million available to cover lost revenue due to the coronavirus emergency.

- Expanded access to U.S. Small Business Administration Economic Injury Disaster Loans: As part of its disaster assistance program, the SBA is providing working capital loans of up to $2 million to small businesses and nonprofits affected by the coronavirus. These loans carry an interest rate of 3.75% for small businesses and 2.75% for nonprofits. Loan repayment terms vary by applicant, up to a maximum of 30 years. The stimulus updated the program so that sole proprietors and businesses with fewer than 500 employees qualify, and applicants don’t need to provide a personal guarantee on loans under $200,000. Payments can also be deferred for up to four years.

According to the SBA, businesses can apply for an Economic Injury Disaster Loan advance of up to $10,000. This money will be in the hands of businesses within three days of completing an application, and does not have to be repaid.

- Emergency grant of $10,000 to SBA Economic Injury Disaster Loan applicants: Even if your business is denied a loan, you can still access this grant, which can be used to provide employee sick leave, maintain payroll or meet other needs like paying rent.

Express Bridge Loans

If you already have a working relationship with the SBA, your business could receive access to loans of up to $25,000 while waiting to hear back on an application for the Economic Injury Disaster Loan.

This Express Bridge Loan Pilot Program was put in place to put money in the hands of businesses as quickly as possible. Once the Economic Injury Disaster Loan application is processed, the money borrowed on this bridge loan will be covered, at least in part, by the amount of money issued to the business in the disaster loan.

FEDERAL INCOME TAX FILING AND PAYMENT DEADLINE EXTENSION

The federal tax return filing deadline is now July 15, 2020. For tax payments of up to $10 million, the IRS has also extended the deadline for both individuals and businesses to July 15, 2020. Estimated tax payments for 2020 originally due on April 15 will now be due on July 15.

Check with your state tax agency to find out if your business has more time to file or more time to pay state and local taxes this year as a result of the coronavirus. Several states have already aligned their tax filing and payment deadlines with the new federal deadline. States also may waive or reduce penalties on late tax payments.

STATE AND LOCAL CORONAVIRUS SMALL BUSINESS ASSISTANCE

States and municipalities are adding programs by the day. Check your governor’s website for up-to-date information about relief available in your area. The National Governors Association offers a list of governors’ websites.

Community funds, which allow residents to donate money to help locals in need, are also popping up. Use the Council on Foundations’ community foundation locator to see if there’s a foundation raising money in your area, and confirm whether small businesses are eligible for grants. You can also check your local news for announcements that a new fund is up and running.

REFERENCES

Clark Howard.com: Michael Timmermann, April 10th, 2020. What You Need to Know About Your Upcoming Stimulus Check. https://clark.com/personal-finance-credit/coronavirus-stimulus-checks/

Clark Howard.com: Nick Cole, April 1, 2020. What’s in the Coronavirus Relief Package for Small Businesses. https://clark.com/business-entrepreneurs/coronavirus-relief-package-small-businesses/?utm_source=Clark+Newsletter+List&utm_campaign=210ed377a9-Clark_Daily_Newsletter&utm_medium=email&utm_term=0_afa92deb83-210ed377a9-73862117

Forbes, March 27, 2020 By Brianna McGurran, Kelly Anne Smith. List of Coronavirus (COVID-19) Small Business Loan and Grant Programs. https://www.forbes.com/sites/advisor/2020/04/03/list-of-banks-offering-relief-to-customers-affected-by-coronavirus-covid-19/#564458174efa

Forbes.com, April 9, 2020 By Robin Saks Frankel. Which Banks Are Accepting Paycheck Protection Program Loan Applications? https://www.forbes.com/sites/advisor/2020/04/09/which-banks-are-accepting-paycheck-protection-program-loan-applications/#5a597df83720

Forbes.com, Robin Saks Frankel, April 9, 2020. Which Types of Coronavirus Relief Can my Small Business Get? https://www.forbes.com/sites/advisor/2020/04/09/which-types-of-coronavirus-relief-can-my-small-business-get/#135023097b1b

Forbes.com, Sarah Hansen, April 7, 2020. After Chaotic Start To Small Business Stiimulus Program, Fed Steps In AS Backstop For Loans. https://www.forbes.com/sites/sarahhansen/2020/04/07/after-chaotic-start-to-small-business-stimulus-program-fed-steps-in-as-backstop-for-loans/#66ab6e783b23

National Governors Association: https://www.nga.org/governors/addresses/

Nerdwallet: Tina Orem. April 10, 2020. Coronavirus Stimulus Check: How Much You May Get and When. https://www.nerdwallet.com/blog/taxes/coronavirus-stimulus-bill-payments/?utm_campaign=ct_prod&utm_source=syndication&utm_medium=rss&utm_term=nasdaq&utm_content=773010

NYtimes.com. Stacy Cowley, April 13, 2020. F.A.Q. on Coronavirus Relief for Small Businesses, Freelancers and More. https://www.nytimes.com/article/small-business-loans-stimulus-grants-freelancers-coronavirus.html

SHRM.Com: Kathy Gurchiek. March 20, 2020. Governments, Large Organizations Offer Help to Small Businesses During Pandemic. https://www.shrm.org/hr-today/news/hr-news/pages/coronavirus-governments-large-organizations-offer-help-to-small-businesses.aspx

Shopify.com: Clark Rabbior. April 5, 2020. Government Relief Programs for mall Businesses Affected by COVID-19. https://www.shopify.com/blog/small-business-government-relief-programs

Techcrunch.com: Anthonhy Ha. March 17, 2020. Facebook announces $100M grant program for small businesses. https://techcrunch.com/2020/03/17/facebook-small-business-grants/